What is a REIT?

Real Estate Investment Trusts are corporations that own and manage real estate. REITs issue units (much like stock shares) that gives investors access to the income generated by the REIT’s property portfolio. Because REITs pass virtually all of its income and gains to investors, REITs don’t pay taxes. Instead, investors pay taxes on the REIT distributions they receive.

REIT in a Nutshell

- REITs allow the average investor to participate in the real estate market through passive investments (through the purchase of company stock or exchange traded funds) and without having to buy and manage properties.

- REITs provide developers an alternative to traditional funding from banks, insurance companies and savings and loan associations.

- Institutional investors and mutual funds use REITs as an easy and liquid way to invest in real estate while providing a quick exit strategy.

- The REITs market is extensive – amounting to $3+ trillion worth of real estate assets[1].

- There are multiple types of REITs – classified by how they are traded (private vs. public), type of assets (equity vs. mortgage) and what sectors they operate in (retail, data-centers etc.).

How REITs Work?

According to Nareit, REITs are modeled on mutual funds, but are backed by real estate properties and/or mortgages rather than stocks and bonds. They all work by assembling a portfolio of assets that back units that they publicly or privately issue to long-term investors through either an initial public offering[2] or private placement. They may raise additional capital through secondary offerings and other means. Each publicly traded unit has a price determined by supply and demand and a net asset value equal to the value of the portfolio divided by the number of outstanding units. Traders can trade publicly traded REIT units directly on exchanges and non-traded REIT units through brokers. Private REITs do not trade publicly.

As an example, Innovative Industrial Properties, Inc. (NYSE: IIPR) is a REIT that manages a portfolio of industrial properties leased to medical-use cannabis facilities. Its IPO[3] occurred on November 28, 2016, when it issued 3.35 million units at $20/unit, a total offer amount of $67 million. It paid $1.55 million in expenses for the IPO. Buyers were subject to a 180-day lockup period before they could sell their units. IIPR sponsored a secondary offering[4] on October 9, 2018 of 2.6 million units at $40 each. As of February 13, 2018, its units traded on the New York Stock Exchange for $65.44 each.

REITs vs Real Estate Investing

There are two basic strategies to make money directly investing in real estate properties. The first is fix-and-flip, in which short-term investors purchase distressed properties, rehab, renovate, repair or redecorate them, and then sell them for a profit, typically within six months to a year. The second is a long-term income strategy of collecting rents. REITs are an alternate way to execute the second strategy, with occasional gains from the sale of properties from the REIT portfolio.

The following table compares publicly-traded REITs with direct investments in real estate:

| ATTRIBUTE | PUBLICALLY TRADED REITs | REAL ESTATE |

|---|---|---|

| LIQUIDITY | HIGHLY LIQUID. You simply sell your units when you want to cash out. | Illiquid. It can take months or years to sell a property. |

| DIVERSIFICATION | REITs provide instant diversification within a real estate sector. You collect rental income from many leases, thereby reducing the impact of any one bad lessee or vacant unit. In other words, REIT diversification contributes to the dependability of income cash flows to investors. You can further diversify you real estate exposure by owning REITs from different sectors. | It takes a long time to build up a diversified portfolio, because most investors add one property at a time, waiting until the latest property’s leasing is stabilized. Overexposed to risk from the vacancy of a single property. |

| INVESTOR COMMITMENT | Relatively small time commitment to select a REIT and monitor its performance. REIT management acts as the landlord. | Large time commitment to lease out and manage your properties and collect rents. |

| MINIMUM INVESTMENT | As low as one unit. | Sizeable capital investment, typically 20% to 40% of purchase price. |

| SHORT TERM GAIN | Only from appreciation of REIT units. | Available through fix-and-flip projects. |

| MINIMUM INVESTMENT | A single share | Usually $1,000 to $2,500 |

| ASSET ALLOCATION | You can quickly adjust your asset allocation to REITs by trading units. | Lack of liquidity makes it difficult to change your asset allocation to real estate in the short run. |

| SHORTING | You can short REIT units to take advantage of a downturn in the real estate market. | N/A |

| PLEDGING | You can pledge all of your REIT units as collateral for another purchase or a loan. | You can only pledge your equity in your properties, and only if permitted by the loan agreement. |

| IRA | Easy to hold in an IRA. | Requires self-directed IRA and a property manager to act as custodian. |

| CONTROL | Your only control is deciding when to buy and sell units. | Complete control over your properties. |

Qualifying As a REIT

For a REIT to qualify as a tax-free, pass-through entity, it must satisfy the following criteria:

- Structured as a corporation or business trust

- Controlled by a board of trustees or directors

- Issues fully transferable units

- Must have at least 100 unitholders

- Distributes at least 90% of taxable income to unitholders

- No more than half of the REIT’s units can be held by up to five individuals

- 75% of assets must be invested in real estate (including rents from real property, sale of real property, and income/gains from foreclosures)

- Receives at least 75% of income from mortgage interest and rents

- 95% of gross income must derive from financial investments (interest, capital gains, dividends and rents)

- Invest no more than 25% of total assets in securities, and no more than 5% of any one issuer’s securities

- Own no more that 10% of any one issuer’s outstanding voting shares

- Limit ownership of stocks in taxable REIT subsidiaries to 20 percent of assets

- Earns no more than 30% of gross income from sales of properties held less than four years

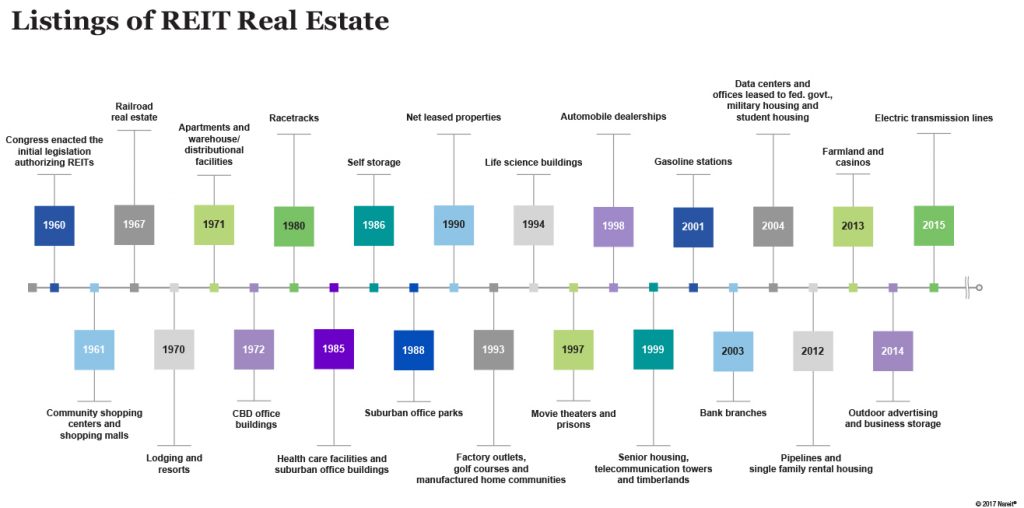

History of REITs

REITs arose from the desire of investors to passively invest in diversified portfolios of income-producing real estate while avoiding double taxation – that is, corporate taxes paid by the REIT and individual income taxes paid by investors. From the 1880s to the 1930s, trusts similar to REITs did provide pass-through income that avoided corporate taxes. However, double taxation was imposed in the 1930s, precipitating a 30-year struggle to reverse this tax regime.

Relief came in 1960 when President Eisenhower signed the Real Estate Investment Trust Act, modelled on mutual funds and allowing investors to invest in diversified, large portfolios of real estate through the trading of public units. In 1961, the first REIT, American Realty Trust, began trading. The idea quickly spread to many countries around the world. Initially, REITs were primarily mortgage companies, investing in the debt used to finance real estate development. Equity REITs soon gained popularity for investors who wanted to receive rental and gain income rather than mortgage payments.

The first REIT index was created in 2001 by the FTSE and Nareit. Today, the Nareit FTSE Global Real Estate Index Series includes almost 500 exchange-traded REITs spanning 35 countries with a market cap exceeding $2 trillion.

The following figure shows when each of the major REIT property sectors were first introduced:

Sources

1) https://www.reit.com/data-research/data/reits-numbers

2) https://www.reit.com/sites/default/files/media/PDFs/NAREIT_IPO_Supplement%20Final.pdf

3) https://www.nasdaq.com/markets/ipos/company/innovative-industrial-properties-inc-1006262-81918

4) https://www.proactiveinvestors.com/companies/news/206425/innovative-industrial-properties-unveils-secondary-offering-to-raise-104m-for-purchase-of-real-estate-assets-206425.html